Understanding AIS and PIS — and how they can boost your business

October 21, 2022 | Hayley Wahlbeck

The second Payment Services Directive (PSD2) is a European regulation that is intended to spur competition in the payment services industry. It facilitates innovative new services that use open banking application programming interfaces (APIs).

Financial service providers need an account information service provider (AISP) license, a payment initiation service provider (PISP) license, or both, to be authorised to use APIs under the PSD2 directive, and they play a crucial role in opening up the financial sector.

Businesses and financial service providers can apply to become AISPs and PISPs themselves, or they can team up with an already-licensed partner, like Aiia. Registered AISPs and PISPs are responsible for complying with the PSD2 rules, including never using the end user’s data for any other purpose outside of the service offered.

Are you considering venturing into open banking in your business? Let’s take a look at what authorised AISPs and PISPs are, the difference between them, and the opportunities they can bring to your company.

What is an AISP?

As the name suggests, licensed account information service providers retrieve financial data from bank accounts to power services with greater insights and accuracy. These providers must receive the account holder's consent to access the information in a read-only format.

What can AISPs do?

AISPs offer tools and services that give customers visibility and insights into their finances based on their transaction data. These tools can include personal finance management (PFM) apps that bring together information from multiple bank accounts into a single dashboard, and into other money management tools. Customers can then use this information to help manage their financial health or to automate manual processes like bookkeeping and reconciliation. AISPs can also use the data to assess a customer’s eligibility for financial products like loans and mortgages, making the decision-making process quicker and easier. This opens up opportunities for AISPs to partner with banks and other financial institutions to develop services that enhance the customer experience.

What is a PISP?

Payment initiation service providers are authorised to initiate payments with the account holder’s consent. In the same way that AISPs gain access to data, PISPs can either connect to bank APIs directly or use a single API from another service provider to connect to multiple banks.

What can PISPs do?

With the ability to initiate payments, PISPs initiate the bank to transfer money in and out of accounts with the account holder’s permission. This allows PISPs to offer financial management tools such as savings apps that automatically transfer money regularly, or services that transfer money between customer accounts to avoid late payments or overdraft fees. For business customers, PISPs can integrate with a company’s back-office systems to manage invoices, make real-time transfers, and increase cash flow visibility.

PISPs also enable e-commerce payment systems that connect directly to a customer’s bank account, increasing the convenience and security of the process by removing the need to enter long credit or debit card information.

Businesses and financial service providers can apply to hold a payment initiation service license or collaborate with another business that is already authorised as a PISP.

Benefits of AISPs and PISPs for your business

Okay, so now you’re fully up to speed on what AISPs and PISPs are, how they link to providing open banking services, and how you can start your journey to offering these to your customers. Now, let’s delve a bit more into how AIS and PIS can really boost your business.

How can businesses benefit from AIS?

The information gathered helps businesses get a better insight into their customers' financial health in a convenient way thanks to reduced manual data entry, and in a more cost-effective way due to reduced administrative costs. With an AIS license, businesses can add value by offering new services, like smart budgeting, helping their customers stay financially healthy and making sure they stay competitive in the market.

What’s more, because customers can share their financial data quickly and securely, AISPs have access to accurate, detailed information to assess their suitability for borrowing. Lenders can use the data to provide tailored decisions on how much a customer can borrow, reducing the potential for loan defaults. This also increases the speed of approvals as it eliminates the need to manually process applications and bank statements, providing a much smoother customer experience.

Another benefit of AISPs in Europe, is that once a customer has passed through the strong-customer authentication (SCA) process, they can then stay logged in to systems for up to 90 days without having to enter their login information again. And abetter customer experience means that businesses benefit from customer loyalty and a strengthened brand reputation.

How can businesses benefit from PIS?

Let’s start with the e-commerce space. The simple and convenient streamlined payment process provided by PISPs creates a better experience for consumers, leading to higher conversion rates for businesses.

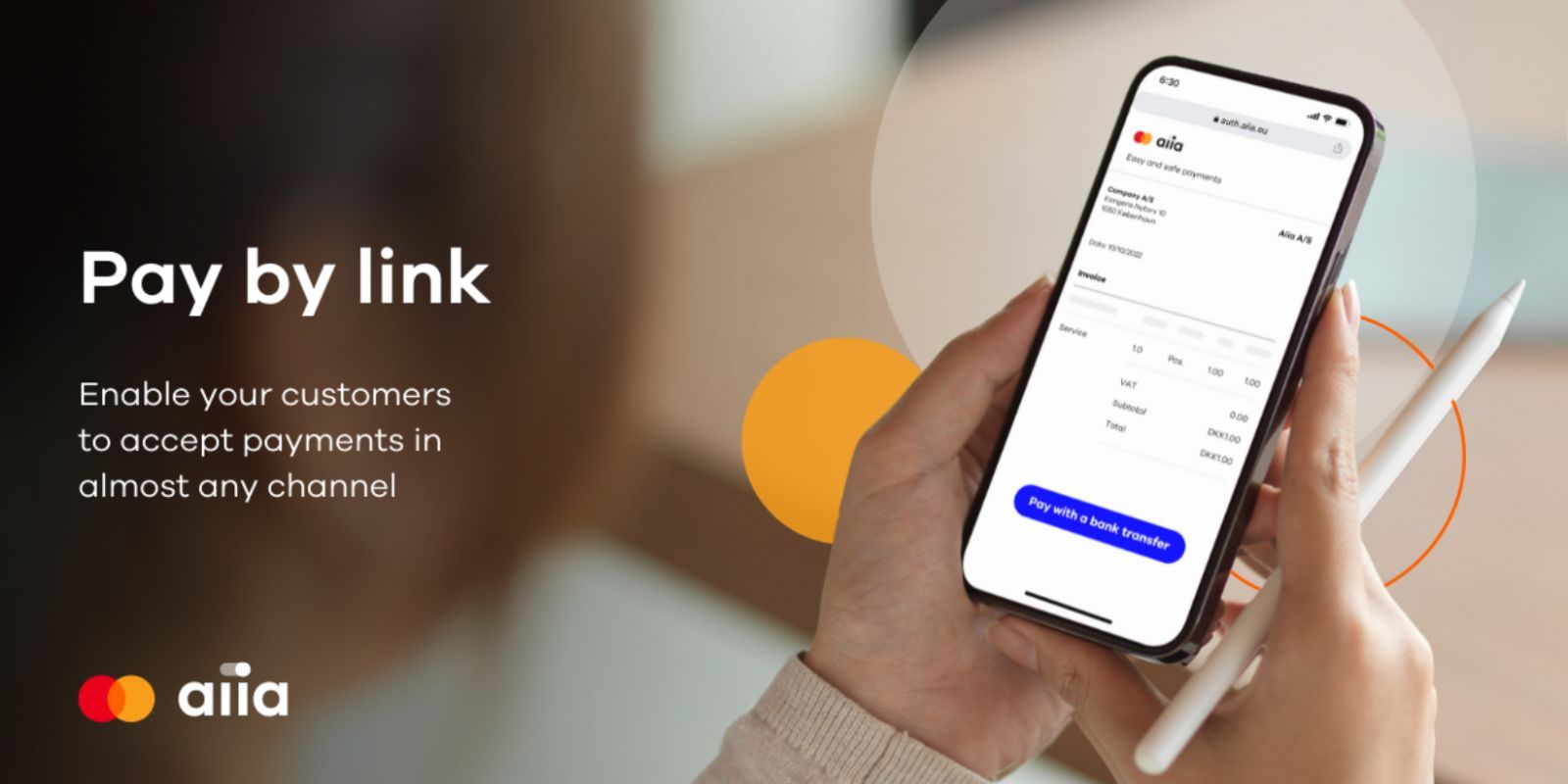

In the accounting segment, PISPs who also have an AIS license enable businesses to build clever reconciliation tools to manage bulk payments of invoices, which saves time and reduces errors. And customers can pay their invoices from wherever they want thanks to features like Pay by Link, increasing the likelihood of businesses getting paid on time.

The big banks who have an AIS license can also benefit from PISPs because they allow the creation of personal finance management tools, and enable customers to transfer money between any of their accounts in their preferred interface.

But don’t just take our word for it…

A great example of AISP open banking in action is Dutch company Tellow which used Aiia’s platform to create an app for smaller businesses to manage all their administrative financial tasks in one place. They can automate bookkeeping, financial forecasting, and expenses right from their app and they can see an overall picture of the financial health of their business.

And as we’ve seen, open banking through PISPs facilitates account-to-account deposits to offer more convenient payment options for businesses. Major Danish commercial pension company Velliv uses Aiia’s payment initiation platform to allow its customers to make payments directly from its self-service platform, keeping things nice and simple.

Learn more about Aiia as your trusted open banking partner

Do you want to learn more about how we can help you open a world of new business opportunities? Contact us to discuss your needs or visit our knowledge hub today.